Introduction: AI is Reshaping Optical Economics

AI isn't coming; it's here. And it is aggressively rewriting the rules of data center architecture. As NVIDIA's latest GPU platforms push interconnect bandwidth to new heights, optical interconnects have become a strategic infrastructure decision, not just a component choice.

According to recent data from Cignal AI, the [800G optical module] segment is expected to be the fastest-growing through 2025. But for procurement leaders, the real question isn't whether to deploy 800G—it's which technology foundation to choose.

The Core Question: Silicon Photonics vs. EML

For years, EML (Electro-Absorption-Modulated Laser) has been the gold standard. However, AI-scale data centers have changed the cost equation. A decisive trend has emerged: Silicon Photonics (SiPh) is rapidly overtaking EML, projected to capture 60-70% of the market share by 2026.

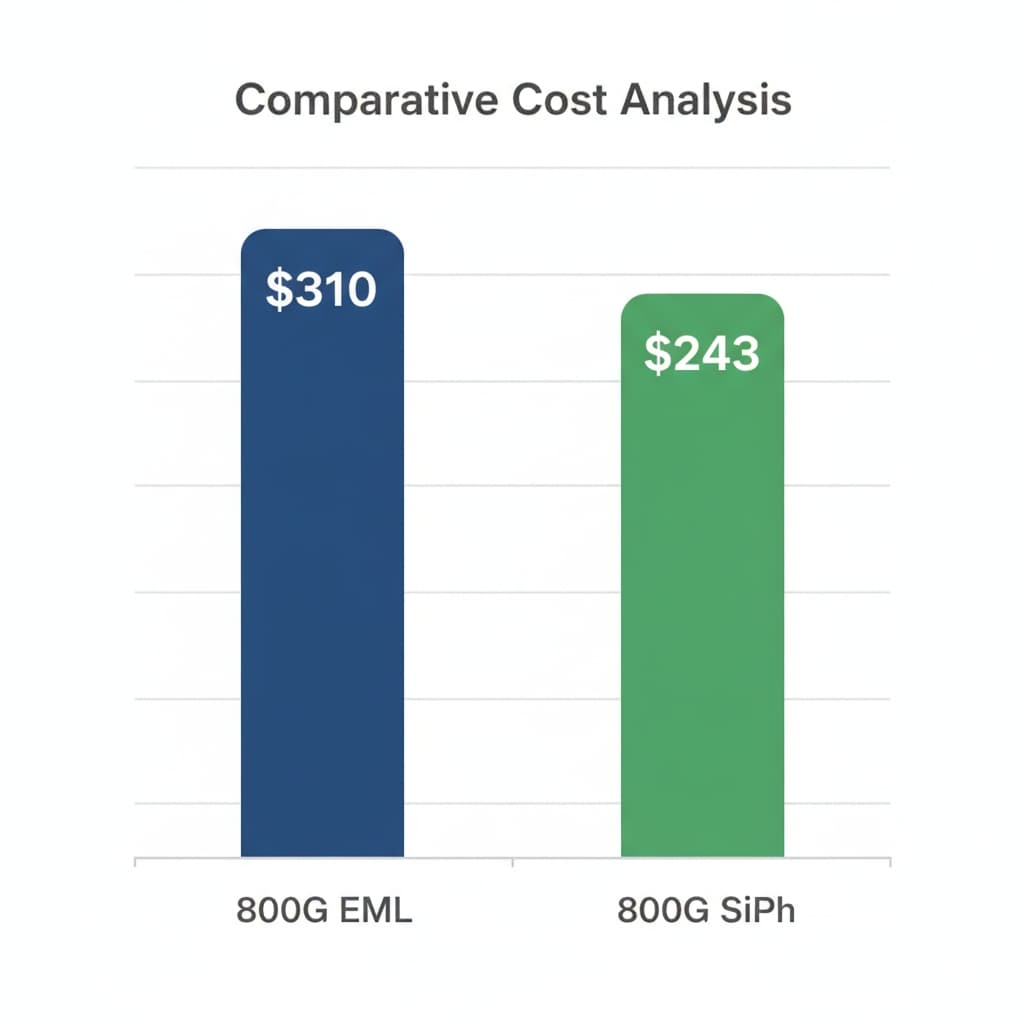

The Economics: A Clear Cost Gap

Based on the latest industry BOM (Bill of Materials) analysis, the cost advantage of SiPh is undeniable:

800G EML Solution Cost: ~$310

800G Silicon Photonics Cost: ~$243

The Difference: ~$67 per module (22% Savings)

This $67 delta is structural. Silicon Photonics integrates modulators and waveguides onto a single chip, replacing complex discrete components found in EML designs. For data center interconnects under 500 meters (DR8)—the dominant use case in AI clusters—SiPh offers comparable performance with significantly lower power consumption and cost.

The Looming 1.6T Supply Chain Crunch

With the 1.6T era driven by NVIDIA's GB200 platforms fast approaching, the argument for Silicon Photonics becomes even stronger due to supply chain security.

The global supply of high-speed EML chips is facing a severe capacity ceiling. Current projections suggest that EML capacity can only meet about 30% of the 1.6T demand in 2026. This leaves a massive supply gap that must be filled by Silicon Photonics, which leverages the scalable CMOS manufacturing ecosystem (foundries like TSMC, GlobalFoundries, and Tower).

What This Means for Buyers

If you are planning your optical infrastructure for 2025-2026, here are three key takeaways:

- Re-evaluate Your DR8 Strategy: If you are still specifying EML for short-reach 800G links, you are likely overpaying. Silicon Photonics has matured enough to be the default choice.

- Secure Supply Chain Early: With the 1.6T transition looming, aligning with suppliers who have secured foundry capacity for Silicon Photonics is crucial to avoiding shortages.

- Look Beyond the Big Names: While Tier-1 vendors drive the technology, agile [third-party suppliers] are now able to offer the same Silicon Photonics architecture at a more competitive price point.

Axonode's Commitment

At Axonode, we don't just watch the market; we adapt to it. We have aligned our product roadmap with the industry's leading Silicon Photonics supply chain to ensure our partners get the most cost-effective, carrier-grade 800G solutions.

As the AI era redefines data center architecture, we are here to help you navigate the transition—from 400G to 800G and beyond.

Real-world Verification: Our lab engineers are conducting rigorous compatibility and traffic testing on high-speed modules (400G/800G) to ensure zero packet loss.

Ready to optimize your network budget?

[ Download 800G Price List ]

800G Silicon Photonics vs. EML: 2026 Cost Analysis & Buying Guide

800G Silicon Photonics vs. EML: 2026 Cost Analysis & Buying Guide

100G QSFP28 Selection Guide: Why Your Link is "Half-Dead" & The 2026 Missing Manual

100G QSFP28 Selection Guide: Why Your Link is "Half-Dead" & The 2026 Missing Manual

The Field Guide to Fiber Optic Network Upgrades: An Engineer's Pre-Procurement Checklist

The Field Guide to Fiber Optic Network Upgrades: An Engineer's Pre-Procurement Checklist

A Deep Dive into High-Speed Data Center Interconnects: A Field Guide for Engineers on DACs, AOCs & Optical Transceivers

A Deep Dive into High-Speed Data Center Interconnects: A Field Guide for Engineers on DACs, AOCs & Optical Transceivers